MTH: Major drill hit - 4.95m at 20.5g/t gold and 1,833g/t silver.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,323,000 MTH Shares and 2,177,000 MTH Options at the time of publishing this article. The Company has been engaged by MTH to share our commentary on the progress of our Investment in MTH over time.

Ultra high grades by any standard...

A 4.95m drill intercept with 20.5g/t gold and 1,833g/t silver.

Inside that was a 0.55m section with grades of 110g/t gold and 7,530g/t silver.

A good time to do it too - gold and silver prices both just keep going up.

Our Mexican gold & silver Investment Mithril Silver and Gold (ASX:MTH) just hit some seriously high gold and silver grades.

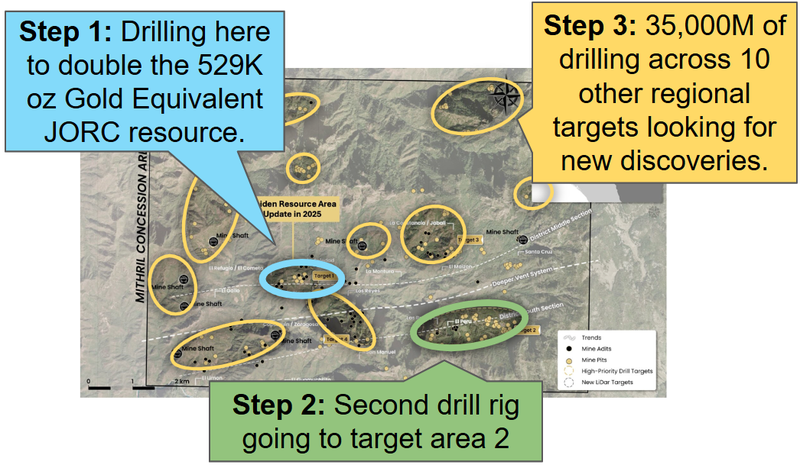

Today’s results are from inside the area where MTH’s 373 Koz of gold and 11 Moz of silver JORC resource sits.

(for context, the existing JORC resource grades for MTH are 4.8 g/t gold and 141 g/t silver)

The results today will go into MTH’s upcoming JORC resource upgrade...

MTH’s target is to double its JORC resource when the upgrade is released to market in the coming weeks.

Drilling in the current target area will also continue until the end of March.

So we should have more results (hopefully like today’s) to look forward to.

And then, shortly after, we get an updated gold and silver JORC resource.

This is from just ONE target area.

MTH has over TEN other target areas that are yet to be drilled.

And $45M capped MTH has $16.7M in the bank - so a big 2025 of drilling coming up.

While the resource upgrade is being worked on, MTH is getting ready to drill regional targets with a second rig.

The second rig is expected to be drilling target area 2 in “early April” - also just a few weeks away now.

After that MTH will be kicking off a 35,000m drill program across its project looking to make NEW discoveries.

This is when things will really get interesting....

That’s when exploration success could multiply MTH’s resource even further.

2024 and early 2025 has been about expanding MTH’s existing resources.

The rest of 2025 is all about adding scale to MTH’s project by drilling for new discoveries.

IF MTH can make a big NEW discovery and multiply its resource base, it should change the way the market values its asset.

The big bonus is that MTH is going into 2025 with a strong balance sheet - $16.7M cash in the bank (including term deposits) at 31 December 2024.

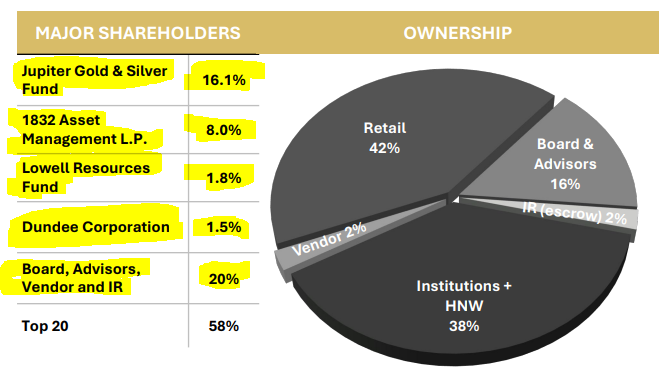

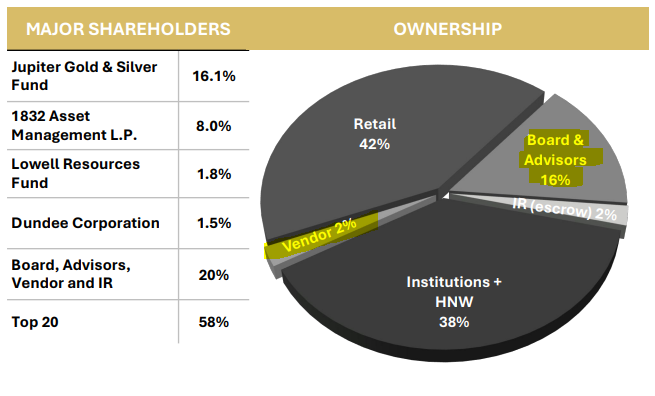

MTH is also backed by a number of big international institutional investors which adds to its ability to drill out its project.

The Jupiter Gold and Silver Fund own ~16%, 1861 Capital own ~8%, Lowell own ~1.8%, Dundee Corp own 1.5% (as at Nov 2024).

That's a decent chunk of the register tied up in funds that typically take a long term view and are investing to see a mine developed.

Over the next 6-9 months, we want to see MTH use that balance sheet strength to:

- Run 35,000m of drilling across regional targets

- Upgrade its JORC resource (maybe several depending on its exploration results)

- Get more drill rigs on site to accelerate exploration.

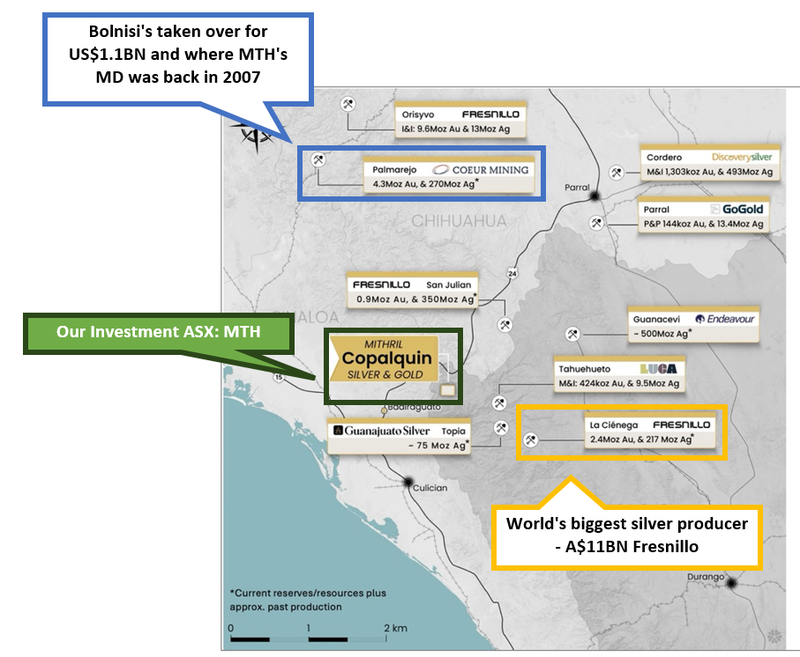

MTH is looking to replicate a US$1.1BN ASX success story

We think MTH has just scratched the surface of its project’s potential.

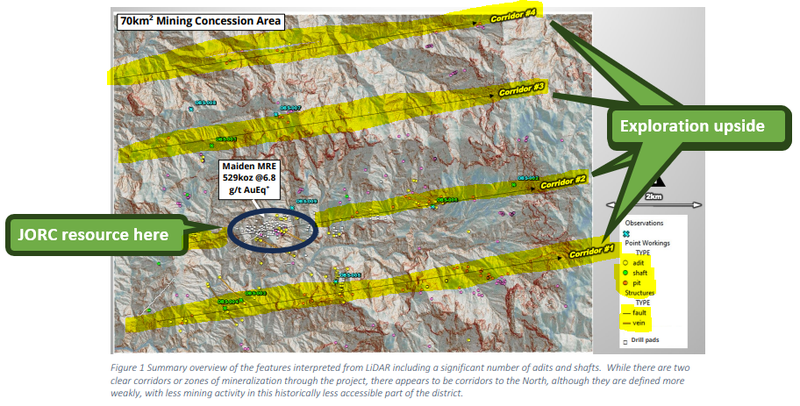

The project sits on ~70km2 of ground where there is evidence of hundreds of artisanal gold and silver mines and workings.

To get an idea of the size of MTH’s project, we have highlighted the four different “vein corridors” that run east to west across MTH’s ground and where the current JORC resource sits:

We think that with some drilling there is a chance MTH finds repeats of its current JORC resource across those corridors.

This was a similar exploration strategy that MTH’s MD John Skeet put to work at Bolnisi Gold ~20 years ago.

(John was the General Manager of Projects with Bolnisi)

We have written about the Bolnisi story several times now, but here is a quick recap for new readers:

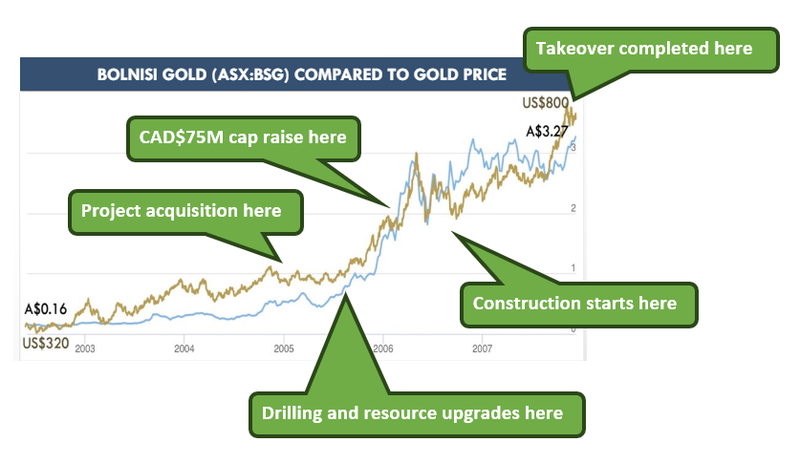

In 2002, Bolnisi acquired the Palmarejo Project in Mexico.

Between 2003 and 2007, Bolnisi and its joint venture partner drilled out the project, uncovering strong gold and silver hits.

Then inside ~18 months of drilling the company made new discoveries and got to a ~3 million ounce gold inferred resource.

Off the back of that exploration success, the company raised tens of millions of dollars and moved its resource into higher confidence categories (indicated/measured).

Then Bolnisi got all of its permits and took its project into the construction phase.

It was at this time that Bolnisi was taken out by Coeur Mining for US$1.1 billion.

In just a few years, Bolnisi share price went up from ~A$0.16 to ~A$3.27.

A 20x return in just three years.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

MTH’s assets were brought into the company in May 2020.

Then Skeet, who was one of the vendors of the assets, joined the company in September that same year.

Below is where MTH’s project sits relative to that US$1.1BN Bolnisi deal, so Skeet should know this part of the world very well:

MTH’s board, advisors and the project vendors now hold ~18% of the company.

We are betting that Skeet with success in Mexico and experience with these types of projects can develop MTH to a point where it becomes an attractive takeover target for a larger company looking to control gold and silver ounces in the region.

With gold and silver prices rallying, he definitely has the right tailwinds to make it happen.

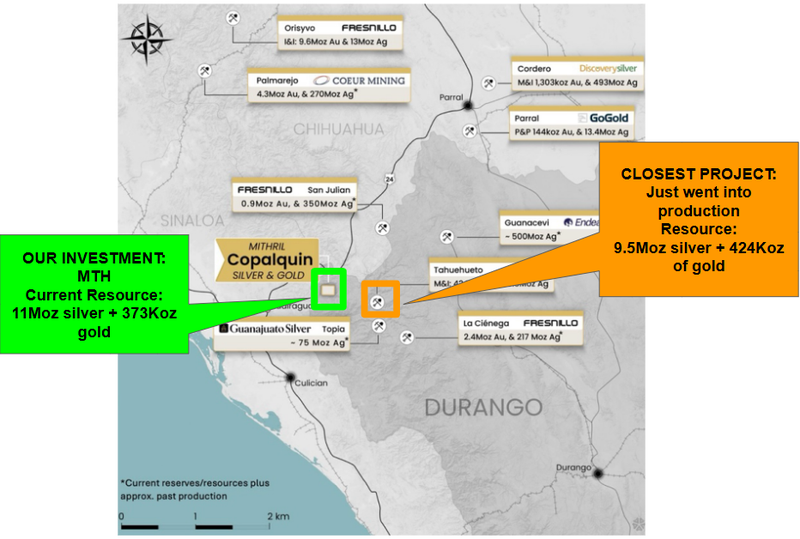

What’s MTH’s closest neighbour in Mexico doing? Going into production...

The nearest gold-silver project to MTH just went into production with a similar sized resource to MTH’s CURRENT resource.

That’s the Tahuehueto mine in the image below about ~1.5kms to the east of Mithril’s project below:

The Tahuehueto mine is owned by Luca Mining a TSX-V listed company and the mine is scheduled to hit commercial production later this year. (Source)

Luca is currently capped at $294M and has another producing polymetallic mine, also in Mexico.

The interesting thing about this for us is that Luca’s Tahuehueto mine has the following resource as of its 2022 Pre-Feasibility Study (PFS):

(Source)

Again, that looks remarkably similar to MTH’s CURRENT JORC resource of 11 Moz of silver and 373 Koz of gold.

MTH is currently capped at $45M.

We think the fact that a mine located that close to MTH, and of that size resource is about to go into production speaks to not only exceptionally high gold and silver prices, but ALSO the long-term viability of MTH’s project.

That viability, in a renowned gold-silver mining jurisdiction, should aid with future financing of the project as MTH moves towards development down the track.

And of course, MTH could have additional exploration upside to unlock across its district scale project over the course of its upcoming 35,000m drilling campaign.

Higher gold and silver prices bring a wave of corporate interest...

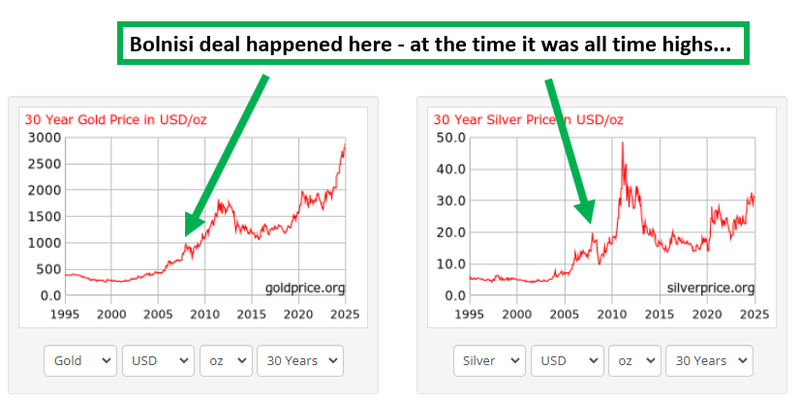

Another similar parallel to the Bolnisi story is that the takeover happened in 2007 when gold and silver prices were trading near all time highs.

In 2007 silver was at around ~US$20 per ounce and gold was ~US$1,000 per ounce.

Both were at all time highs...

The Bolnisi deal got away just before the Global Financial Crisis (GFC) came, and silver and gold prices crashed.

What happened next was the more interesting thing though... gold and silver prices rallied again and hit much much higher all time highs.

We think there is a chance gold and silver could be on the cusp of a similar rally.

There was a COVID spike for gold and silver, a small retracement for a few months and then now what looks like the start of a new rally.

We have been talking about a wave of M&A that we thought would happen across the gold space for over a year now.

Our view was that as the majors make a ton of cash while gold prices are high, they would first consolidate and get even bigger.

AND then look further down at the mid/small caps for takeover targets.

(it's no surprise that the Bolnisi deal happened when gold was at all time highs... the majors would have been making huge amounts of cash).

Here is the order of events we said we expected to see as the gold price continues rising:

- Majors with producing assets start to make record profits - we can see this happening in the recent quarterly reports of the producers. Some have had EBITDA quadruple...

- Majors then look to do M&A deals (first between each other, then in the mid cap space) - the Newcrest, Newmont deal was the trigger back in 2023. Then in 2024 the deals got more and more into the mid caps space.

- Eventually M&A begins at the small/mid cap space - Now in 2025 we are starting to see the bigger players come in and pick off the small caps (The ~$110M AngloGold deal with Matsa is a good example of this).

We think that the M&A cycle is now firmly in that third stage.

AND there is precedent for big deals happening on Mexican silver/gold projects.

Late last year A$4.1BN New York/Canadian listed First Majestic bought out Mexico based Gatos Silver for US$970M.

A proof point for us that IF a project can get big enough there is corporate interest in Mexican silver/gold projects.

(Source)

So why do gold and silver prices matter?

Ultimately, the markets are a function of capital moving around looking for a home (and a return).

If gold and silver prices are going up, then whatever MTH is able to find and put into its JORC resource becomes more valuable (and potentially more economical to mine).

As a resource gets bigger, it adds economies of scale and once it hits a certain size/scale it starts to become a project that can be developed and mined.

Gold and silver prices are also what draw investor attention to projects with genuine size/scale.

A combination of corporate cash and market capital flows impacts share prices and the valuations these companies trade at.

We think that where gold and silver prices are and the market's appetite for gold/silver projects will be what impacts whether or not MTH is able to achieve our Big Bet which is as follows:

Our MTH Big Bet

“MTH re-rates to a $150M market cap by expanding its Mexican gold-silver resource with new ultra high-grade silver (and gold) drill hits, taking the project into development and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MTH Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What is next for MTH?

🔄 Additional assays - MTH is currently drilling in and around its existing JORC resource at Target 1, we are looking forward to more assays from ‘Target 1’ over the coming weeks.

🔲 Double JORC resource - This would enhance the scale of MTH’s project and make it more attractive as an investment for larger funds and increase its standing among precious metals projects around the world.

🔲 Drill out other targets - MTH has 35,000m of drilling planned for this year. Once all of the drilling is complete over Target 1 it will move to drill out other targets in the district.

Risks to MTH’s share price in the short-term

With drilling currently underway and more assay results to be published over the coming months, we think the key risk in the short term for MTH is “Exploration Risk”.

It’s possible that MTH is unable to find enough significant economic mineralisation, which we think could impact the scale of its planned resource upgrade.

If the resource upgrade fails to deliver relative to market expectations, then we would expect MTH’s share price to react negatively to the news.

Exploration risk

There is no guarantee that MTH’s upcoming drill programs in Mexico are successful. MTH may fail to find economic silver-gold deposits.

Source: “What could go wrong” - MTH Investment Memo 22 May 2024

We list more risks to our MTH Investment Thesis in our Investment Memo (link below).

Our MTH Investment Memo

You can read our MTH Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our MTH Investment Memo covers:

- What does MTH do?

- The macro theme for MTH

- Our MTH Big Bet

- What we want to see MTH achieve

- Why we are Invested in MTH

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.